Note to reader: I added the charts and captions for emphasis, editorial content, and clarity.

I do find it interesting that when the Fed cuts overnight rates, longer dated real yields rise. I have enumerated my theories previously as to why this is the case. This article touches on some of my previous thoughts.

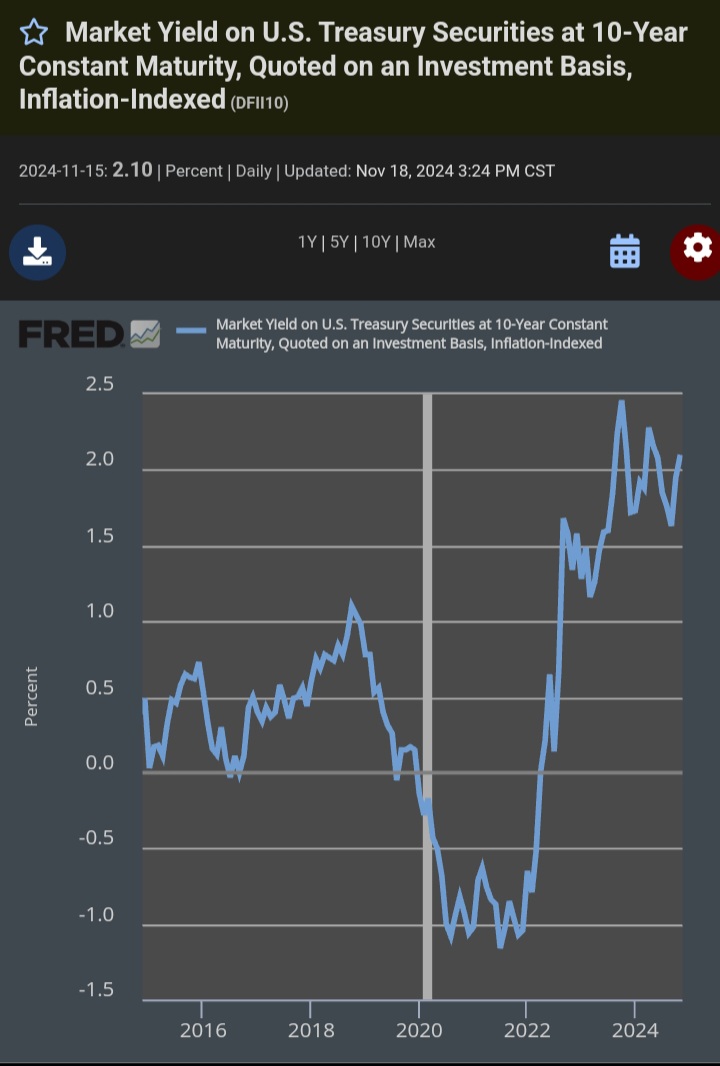

Quantitative easing (QE) can no longer be practical if Fed Treasury buying is accompanied by higher price inflation. This wasn’t the case last decade as QE operated as designed. QE worked to subsidize real borrowing costs, despite unprecedented fiscal deficit growth.

As we can see from the charts below, this is no longer true. The FED is cutting short-term rates and backstopping much of the credit markets in an unprecedented fashion, yet longer dated real yields are rising.

Bond investors are no longer willing to subsidize government malfeasance and are gradually concluding that the Fed may have lost many of its previous abilities. In essence, bond investors are demanding a higher risk premium, which manifests in higher real bond yields across the curve.

It’s important to note that asset prices may continue to climb if investors believe that the government’s financing abilities have been effectively curtailed and pose a further credit risk.

The Fed is losing its ability to subsidize government borrowing costs

But it’s highly possible that the current nearly 4.5% nominal yield on the 10-year, and well over 2% real rate, will stay in those ranges for a simple reason: Investors are getting increasingly worried about gigantic budget deficits exceeding 6% of GDP that can only get worse if Trump delivers on his pledge to radically slash taxes.

Donald Trump’s landslide victory has sparked a sharp jump in stock prices, and unleashed a wave of optimism that big cap equities, after already posting enormous gains this year, could keep pushing to new highs. In the nine days following the election, the S&P 500 surged over 4% to notch an all-time record close of 5949 on Thursday, November 14. Even after a big drop to end the week, the big cap index is still up over 3% since Trump clinched his overwhelming win. The business press is buzzing over Wall Street’s great expectations for the Trump agenda that incorporates such pro-business proposals as slashing the corporate income tax and fostering a ramp in energy production. On November 18, a front page headline in the Wall Street Journal trumpeted that “Investors are Betting on a Market Melt-Up.” The story related that money’s pouring into equity funds at a rate rarely witnessed since the onset of the Great Financial Crisis.

But the media and the average folks and money-manager whales wagering on flush times ahead are missing the big overlooked story: The shocking, sudden rise in interest rates. This explosive shift, in the wrong direction, for a crucial long-term driver of stock returns is sending exactly the opposite message from the jubilation spread by the prospects for a second Trump term. As Warren Buffett has warned time and time again, bonds compete with stocks for investors’ money, and when super-safe fixed-income provides puny yields, stocks, based on fundamentals, can be worth a lot more. Well, bonds just got far more lucrative overnight, for potentially worrisome reasons, and the outlook for equities just got a lot worse. But for now, animal spirts are swamping the bedrock basics that, over time, inevitably guide valuations.

The 10-year just took one of its biggest quick leaps in history, a bad omen for stocks

On October 1, the rate on the 10-year treasury bond, the fixed-income benchmark that exerts the strongest influence on equity valuations, stood at a highly-favorable 3.74%. The rate had dropped steadily from over 4.64% at the close of May. Expectations that yields would remain extremely modest well into the future kept the powerful rally in stocks on track.

Then, that balmy trend turned stormy. By Monday, November 18, the 10-year yield had vaulted to 4.47%, a stunning increase of 73 basis points in just over six weeks. A big part of that jump happened following Election Day. The increase came in two parts: the rise in the “inflation premium,” and a waxing “real yield.” Neither one is good for stocks. The “inflation premium” measures investors’ expectations for average yearly increases in the CPI over the next decade. That component rose from 2.19% to 2.33% since the start of October. Takeaway: Investors are fretting that the Fed’s restrictive policies will take a long time to wrestle inflation to their 2% target, and may even fall short. In any event, the rise in the inflation premium signals that the central bank may need to hold short-term rates high for an extended period. And any sign the Fed will remain tighter, for longer, is a curse for equities.

The second part, the upward trend in the “real yield,” accounted for a much bigger share of the total rise, swelling from 1.56% to 2.15% and contributing 59 points of the 74 bps total increase. That’s an even darker warning than the prospect that inflation may prove stickier than anticipated. It’s the “real” number that exercises a gravitational pull over equity valuations. The inflation-adjusted yield reigns as the so-called discount rate applied to a company’s expected flow of future earnings to determine its “present value.” It’s a staple tenet of financial analysis: The higher the discount rate, the lower the value of those profits looming over the horizon, and hence the less you should be paying for the stock.

But the the real yield’s steep ascent didn’t hammer share prices. In fact, the markets just kept humming as November 5th approached, then took another leg up when Trump proved victorious. The rub: It’s extremely low real rates that have supplied the biggest tailwind to two-decade-old bull market. From 2014 to 2022, inflation-adjusted yields averaged an extraordinarily favorable 0.8%. The market clearly bought the view that the real rate would stay low for years to come, justifying high PE multiples.

As of November 18, the PE on the S&P 500 stands at 29.4, based on the trailing four quarters of GAAP reported earnings. That’s a number you’ll seldom hear from Wall Street, and it’s the biggest since the tech bubble ended in 2002, except for brief periods during the Great Financial Crisis and Covid-19 outbreak where earnings collapsed, artificially inflating multiples. At those sumptuous valuations, what edge do stocks offer over bonds? The expected return on equities is the inverse of that 29.4 PE, or 3.4%. The expected real return on the 10-year is that real yield of 2.15%. Hence, stocks, the high-risk, volatile choice, especially at these prices, are positing a measly spread of 1.25 points versus the super-reliable treasury bond. Compare that narrow margin with the over three times bigger, 4.4 point cushion that equities enjoyed in mid-2021, when the real rate was negative 0.3%, and the S&P’s PE hovered at 24.6, a relative bargain compared to its current level of nearly 30.

Of course, the bulls will argue that an explosion in earnings, courtesy of the Trump deregulatory and tax-lowering program, will keep propelling the markets. The math exposes that outlook as highly unlikely. Profits are already stagnating following a bubble that grew between 2016 and 2021, when S&P earnings-per-share exploded 110%. In the past 11 quarters, EPS has risen only 2% overall, a number that trails inflation by a wide margin.

The big question is whether the leap in the real rate represents a structural shift or a mere blip that could reverse as fast as it ramped. We don’t know the answer. But it’s highly possible that the current nearly 4.5% nominal yield on the 10-year, and well over 2% real rate, will stay in those ranges for a simple reason: Investors are getting increasingly worried about gigantic budget deficits exceeding 6% of GDP that can only get worse if Trump delivers on his pledge to radically slash taxes. All we know is that the one force that more than any other has boosted stock prices over the last decade or more, extremely low interest rates, just did an astounding about face. The safest part of the market, U.S. treasuries, offered no competition for stocks for many years. That scenario’s totally changed. Maybe that’s one reason Buffett is lightening up on equities and buying U.S. government bonds. Hope not math is now driving the markets. And in the end, it’s the math

that always wins.

Target 🎯 TGT taking a huge dump pre-market. Down $27.

Seems like all the businesses that depend on the lower end consumer are suffering while those that depend on the high end consumer are doing better. Clearly a growing rift between the haves and have nots.

Isn’t it the other way around? Walmart (WMT) has almost doubled over the last year where Target has stayed the same.

WMT is absolutely rocking! The next trillion dollar company? We all feed the beast.

Own the income generating assets….

Bridgewater Says Trump May Pick More Accommodating Fed Chief

(Bloomberg) — President-elect Donald Trump’s policies on tariffs, fiscal stimulation and immigration will likely push the US toward missing its 2% inflation target, Bridgewater Associates Co-Chief Investment Officer Bob Prince said on Wednesday.

Should US inflation move closer to 3% in about one a half years from now, Trump may be inclined to nominate a Federal Reserve chairman who would accommodate the higher target and free him to cut interest rates, he said at Hong Kong’s third annual Global Financial Leaders’ Investment Summit.

“There is a desire for cutting interest rates,” he added. “But if the inflation rate holds up, then that can preclude cutting rates, which I think sets up an interesting situation 18 months from now” when current Chair Jerome Powell’s term expires.

Prince is joining peers who have warned investors to brace for higher inflation under a second Trump presidency, with its promises of pro-business and pro-growth policies adding pressure on prices and constraining labor force expansion.

“Investors should still consider putting their money in the assets with strong inflation protection,” John Studzinski, vice chairman and managing director of Pacific Investment Management Co., said separately at the Forbes CEO Conference in Bangkok.

“Inflation won’t go away, while proposed tariffs by the US will affect the prices. Geopolitical risk in the Middle East is also the main risk for supply chain and logistical costs,” Studzinski said.

Trump has criticized Powell, who has said that he wouldn’t leave his post if asked to resign by Trump. Powell said in a briefing earlier this month that any attempt to demote him or any other Fed governor in a leadership position was “not permitted under the law.”

The Fed chair has said the recent performance of the US economy has been “remarkably good” and has not sent any signals that policymakers should be in a hurry to lower rates.

Monetary policy could face headwinds next year if Trump fulfills his campaign promises to cut taxes, restrain immigration and deploy tariffs.

Trump’s policies would likely create an economic scenario of higher nominal growth, with spending staying higher and the yield curve trending steeper, Prince said. Household balance sheets are in “pretty good shape,” helped by prior decades of deleveraging, he said, adding that solid wages mean the spending has been largely financed by income, not credit.

Combining that with fiscal stimulation, investors may not get the real interest rate cuts they were looking for before. That environment is more favorable for equities, as companies with pricing power can turn that nominal spending into nominal earnings growth, Prince said.

The challenge in the equity market is that investors have not only priced in the best decade for corporate earnings in the past 10 years, but have fully factored in the probability of it happening again, Prince added.

I have not flown an airline in over a decade. I am no longer flying commercial ever again. Trips are expensive and since I don’t work for people nor run a business, every day is a vacation for me. Millennials May own a home, but it will be matched with a huge mortgage. Trips are expensive. My wife flew to Vermont last month for a two night trip to visit her brother and it cost $1,200, and the brother chauffeured her around and she stayed at a local motel where he lives. No thank you, I stayed home.

——–

Delta Sees Premium Tastes of Millennials Boosting Profit Margins

Mary Schlangenstein

Millennial travelers are spending more on air travel than all other generations, according to Delta Air Lines.

(Bloomberg) — Delta Air Lines Inc. expects profit margins to swell through the late 2020s as the airline leans into demand for premium travel and the millennial customers willing to pay for it.

Operating profit margin should reach a mid-teens percentage between 2027 and 2029, above Wall Street expectations and the roughly 11% the carrier expects this year, Delta said in a statement outlining long-term financial targets on Wednesday. The carrier expects free cash flow to increase to as much as $5 billion annually in that time frame, up from the more than $3 billion the company anticipates this year.

The outlook highlights how Delta sees continued gains on the horizon from its aggressive push into upscale travel experiences and products that many rivals are now seeking to replicate. The carrier plans to offer more premium seats in its aircraft fleet, with sales from those classes expected to exceed economy tickets by the end of 2027, it said. At the same time, the airline will keep offering some cut-rate basic economy fares to lure travelers away from deep-discounters.

“We’ve been at it for 15 years, investing aggressively,” Chief Executive Officer Ed Bastian said in a briefing with reporters.

Delta expects millennial travelers to buy many of those pricier tickets. That group — people generally born between the early 1980s and mid-1990s — is spending more on air travel than all other generations, and about two-thirds are willing to pay for luxury travel, the carrier said.

About 85% of the seats Delta plans to add in 2025 will be premium, Chief Financial Officer Dan Janki said. Delta will also use Airbus SE’s A350-1000 widebody jet for its longest international flights after deliveries begin in 2026. About half of the plane’s cabin will be comprised of premium seats.

The carrier intends to further divide each fare class to offer more opportunities to add features for an additional cost, Delta President Glen Hauenstein said. The airline’s not worried about a backlash, he said, because history has shown that customers are not disappointed so long as ticket features are not being taken away.

The airline is also banking on continued reliability, technology investments and its co-branded credit card program with American Express Co. to help fuel sustained profits. Payments from American Express for loyalty points to award to members should reach more than $7 billion this year and $10 billion annually long term, Delta said.

Near-term, Delta expects revenue in 2025 to grow in the mid-single digits, compared with analysts’ expectations for about 6.1%. Non-fuel costs to fly each seat a mile, an industry gauge of efficiency, will increase in the low-single digits, Delta said. Analysts were expecting a 1.3% decline.

Flying capacity next year will increase as much as 4%, Delta said, compared with a 4.3% decline expected by Wall Street. A deluge of aircraft seats in the domestic market damped fares during the busy summer travel season and led several carriers to cut capacity since August.

I have not flown on a commercial airline for 14 years and I refuse to do so. The US airlines treat the average passenger like cattle unless you pay a huge premium such as business or first class.

If you want to fly comfortably then you have to really pay up. In addition, there are shoddy planes and long flight delays.

I use to love flying on a commercial jet while growing up back in the seventies as the planes were comfortable then and the airlines made sure all their passengers were treated well.

It seems like millennials prefer to spend lavishly on vacations as opposed to saving and investing in income producing assets. Delta airlines is counting on big spenders.

Yes, flying is too expensive, too crowded with numb skulls and too much hassle!

Everything Has Changed Now’: Biden Spends Last Months In Office Gambling Risk Of Nuclear War With Russia

https://dailycaller.com/2024/11/19/joe-biden-risks-escalating-russia-ukraine-war-us-missiles/

Now the British have joined in. Ukraine’s armed forces fired British cruise missiles at military targets inside Russia for the first time, a Western official familiar with the matter said.

Trump’s pick for the UST Secretary will obey and print. Asset owners rejoice.

Money Printer To Go Brrr

https://youtu.be/O1hCLBTD5RM?si=qvfFtAXjrqXhUtay

Rowan will make the Fed open the printing presses….

Trump to interview Warsh, Rowan for Treasury job on Wednesday, Bloomberg News reports

https://www.reuters.com/world/us/trump-interview-warsh-rowan-treasury-job-wednesday-bloomberg-news-reports-2024-11-20/

(Reuters) – U.S. President-elect Donald Trump is scheduled to interview former Federal Reserve Governor Kevin Warsh and Apollo Global Management (APO.N), opens new tab CEO Marc Rowan on Wednesday for the post of Treasury Secretary, Bloomberg News reported on Tuesday, citing people familiar with the matter.

The Financial Times separately reported, opens new tab on Tuesday that Rowan has emerged as a top contender for the Treasury job, citing several people familiar with the matter.

Lets say it together, Marc Rowan is …

The federal government continues to allow its fiscal deficits to grow, while the yield curve continues to remain elevated on a real basis. The $1.4 trillion dollars in Treasury interest income that’s generated is lining the pockets of the asset owners while destroying the wage slave.

To wit, GDP growth continues to look good and the economy on a macro basis continues to look mighty fine. I just raised rents on a couple of my properties and income streams continue to climb. Soylent Green can be profitable, but it just depends on which side of the equation a person finds himself.

Russian Ruble Falls to 13-Month Low After Ukraine Missile Strike

Bloomberg News

A weaker ruble isn’t a concern now and will benefit the state budget amid plans for increased spending next year.

(Bloomberg) — Russia’s central bank set the ruble’s exchange rate at more than 100 per US dollar for the first time in more than a year after Ukraine used US-supplied missiles to strike in Russia for the the first time.

The Bank of Russia has used interbank transactions to calculate the rate since June, when the US sanctioned the Moscow Exchange — which immediately halted dollar and euro trading. Still, the national currency has been steadily falling against the greenback for weeks and weakened slightly to 100.0348 per US dollar, data from the Bank of Russia showed Tuesday.

Eastern European assets were buffeted after President Vladimir Putin approved an updated nuclear doctrine that would allow Russia to use nuclear weapons in response to a conventional attack on its soil that threatens its sovereignty.

Overnight, Ukrainian forces carried out their first known strike in Russia using Western-supplied missiles, attacking a military warehouse in the Bryansk border region.

A weaker ruble isn’t a concern now and will benefit the state budget amid plans for increased spending next year, two people with knowledge of the situation earlier told Bloomberg. Officials expect the ruble at an average level of 96.5 per dollar in 2025 compared to an average 91.2 per dollar this year, a forecast from the Economy Ministry showed.

Russia’s currency twice weakened past 100 against the dollar last year, with the first instance prompting the Bank of Russia to hold an emergency meeting to hike the benchmark by 350 basis points. The government imposed capital controls to ease pressure on the ruble after it fell below the 100 level in October of last year.

In the immediate aftermath of the February 2022 invasion of Ukraine, the ruble also weakened to around 120 per dollar, but quickly rebounded.

The ruble also slightly declined against the Chinese yuan to 13.7744, according to the central bank.

Warren Buffett has been decreasing his stock position for a while now and if the Fed is losing control of the yield curve, whether by design or not, (I say by design), look out below. I remember when Trump ran the first time and won, I wondered if they would give him the Herbert Hoover treatment. Maybe this time they will!

The one thing this Fortune Magazine article gets wrong is by indicating that Warren Buffett is buying treasury bonds. He is not. He is parking all of his cash in short-term treasuries with durations of a year or less. I suspect he’s only buying t-bills.

This is different this time around. The asset markets could continue to move higher as faith in the federal government’s ability to finance continues to be undermined and as confidence in the Federal Reserve continues to dwindle.

By the time the MSM tells us the Federal Reserve has lost control it would be way too late and asset prices will be much higher than they are now. It will be too late to buy a house and to do a lot of things.

The reports are currently big on Powell’s dovish attitude, rate cuts and that soft landing news.

Powell and the FED are definitely dovish. They keep cutting rates, despite the cost of living remaining bone crushing for those who don’t own the assets. I have mentioned previously that my calculations indicate a neutral fed funds rate of at least 4%.

The stock market and the monetary type of assets like gold and Bitcoin are doing very well in spite of higher Bond yields and overnight rates.

If we think about how much the federal government is paying out in interest, which is about $1.4 trillion annually on the run rate, that’s a lot of money being put into the pockets of bond and money market holders.

And it seems the threat of nuclear war sends investors into treasuries which lowers the yield also!

Certainly out of the Russian ruble. Despite all this talk of war, Treasury yields aren’t really dropping. I think War actually is causing problems on the yield curve, because investors are wondering how this war buildup will be paid for.

Very good analysis. At the end of the day reality always wins. Imagine what it will be like when reality sets in after 30 or more years of fantasy where stocks and bonds defied reality. It’s going to get ugly.