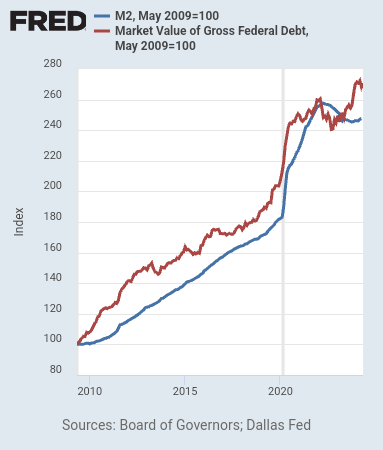

M2 growth has roughly mirrored total UST market value growth since QE commenced

In some of your posts you’ve highlighted a reduction in the money supply by some metrics while also showing the continually expanding debt which in the short term appear to be at odds on some level. Do you think the reduction in the money supply might be enough to trigger a short term stock market pullback (maybe by early fall), which could then be used to justify a return of QE under some guise?

N

If we take a look at the next few charts, we can see that the money supply is not shrinking, but rather stabilizing at a rather high level. The same is true for the Euro area. Taken further, we can observe the explosion in the US Treasury debt measures as well. Of course, all this covid stimulus was ultimately just an excuse to greatly accelerate fiscal deficit spending, which resulted in the elevated price inflation measures we are currently observing. All this additional spending and money is still rippling through the economy as much of it was not effectively sterilized. However, as time goes on, all of this spending is being captured by the largest firms as profit. This huge soaking up is still taking place.

About the time that the covid stimulus was first announced in March and April of 2020, I instructed the reader to buy as many income generating assets as possible, because all of this sovereign debt generation would result in higher asset prices across the board. Compounding the misery for the average person is the fact that the Federal Reserve waited too long to attempt to control the growing price inflation that resulted.

As the months move forward from here and the money stock measures stabilize, inflationary pressures should and have been coming down. Of course, we still have trillion dollar deficits, which must be financed with additional sovereign debt securities. These sovereign debt securities provide investors with collateral to purchase other assets, such as the national housing supply as well as equities and marquis businesses.

With short-term interest rates remaining elevated, the level of federal government interest expenses continues to climb at a rapid pace. While the small saver can park money in Schwab’s money market fund at 5.2% and make some extra cash, the vast majority of this extra money the federal government is paying for its financing is going to the institutions. This essentially is another great transfer of wealth vehicle from the taxpayer and wage earner to the institution. As we can see, this interest expense has now crossed the trillion dollar threshold.

In essence, this is additional money that ends up in the pockets of the large institutions and it is being used to purchase more assets and consolidate the wealth. The wage earners are the last ones to see this extra money and by the time they see it, the cost of living has already increased to the point that any extra wage is spent. Those who see this money first are the ones who benefit. The asset owners benefit through higher levels of asset price appreciation and the ever increasing cash flows these assets generate. Stock owners have been richly rewarded as the Federal Reserve subsidizes this wealth transfer by suppressing bond yields. Existing homeowners benefit as the prices of their homes escalate.

Asset owners easily stay up with inflation while wage earners and fixed income recipients continue to fall further behind. Extended periods of elevated inflation continue to widen the distance between the asset owners and the wage earner and benefit recipient. For asset owners, inflation does the heavy lifting to increase their wealth.

Eventually, this stage of the wealth consolidation process will have to shift. I don’t know what the catalyst will be, but the federal government cannot continue spending over a trillion dollars a year on interest expense indefinitely. Something has to give. Thus, I figure that a modification to the wealth consolidation plan is in the cards and that some sort of exogenous set of circumstances could play out. This set of circumstances could provide the catalyst for the Federal Reserve to lower interest rates once again.

If the Fed lowers interest rates, USTs will no longer be as attractive to investors and those parking cash overnight in government Treasury bills will seek other investment choices. Thus, the Fed will need to begin expanding its balance sheet once again if interest rates fall.

As of now, the Fed does not have any justification for expanding its balance sheet. Of course this is linear thinking. Economic measures are still relatively robust and price inflation is still elevated. The problem with the Fed’s misguided monetary policy is that it keeps announcing to the public that it intends to lower interest rates eventually and because of this, it is effectively loosening monetary policy without actually doing so. Moreover, this trillion dollar level of federal interest expense continues to bleed into the CPI measures as much of this money is also spent by the public.

The Federal Reserve has done a lousy job sterilizing all of this additional money, but as all of this additional spending continues to be consolidated onto the balance sheets of the wealthiest, inflation will eventually abate. The wealthy do not spend as much of their income on the cost of living as the poorer people do. Nevertheless, the Fed will need to do something as the cost of living becomes too onerous and house prices continue to move higher, regardless of mortgage rates. Essentially, something has to give and the Federal Reserve needs an excuse to drop interest rates, which will then provide the catalyst to expand its balance sheet. In a sort of ironic twist, lower interest rates could actually assist in lowering price inflation as the federal government should see lower interest expenses.

Under the QE system, asset prices win out in every scenario and the wage earner, by definition, falls further and further behind as the months and years drag on. These dynamics are just functions of one another.

3 thoughts on “A reader asks; could a drop in the money supply trigger a stock pullback and more QE?”

I am so grateful I began investing out near Strasburg, Winchester, and in Shenandoah County Virginia. This area is on fire because it is mostly Caucasian European and they have a long heritage. Conservative Caucasian money is bailing on the multicultural garbage dumps near DC and deploying it out here in droves. I now have six houses here and can’t wait to dump more PG County properties.

To wit, according to The Hill, the Shenandoah County School board reverted the names of two of their schools back to their former Confederate names before the blacks cried out to their debt slave owners for action.

“Confederate names make comeback, triggering lawsuits”

A Virginia school district was sued this week after it restored Confederate military names for two buildings, foreshadowing a broader battle that is heating up ahead of the election.

The Virginia NAACP sued the school board in Shenandoah County after it voted to change Mountain View High School to Stonewall Jackson High School and Honey Run Elementary back to Ashby Lee Elementary.

Thanks for another thorough analysis keeping your readers up to speed… I’ve read this a few times and I’m not finished yet. Further to your comment re: finding buyers for US debt, notice the saviour being forecast in this article as the digitization of the dollar advances

If we take a look at the next few charts, we can see that the money supply is not shrinking, but rather stabilizing at a rather high level. The same is true for the Euro area. Taken further, we can observe the explosion in the US Treasury debt measures as well. Of course, all this covid stimulus was ultimately just an excuse to greatly accelerate fiscal deficit spending, which resulted in the elevated price inflation measures we are currently observing. All this additional spending and money is still rippling through the economy as much of it was not effectively sterilized. However, as time goes on, all of this spending is being captured by the largest firms as profit. This huge soaking up is still taking place.

If we take a look at the next few charts, we can see that the money supply is not shrinking, but rather stabilizing at a rather high level. The same is true for the Euro area. Taken further, we can observe the explosion in the US Treasury debt measures as well. Of course, all this covid stimulus was ultimately just an excuse to greatly accelerate fiscal deficit spending, which resulted in the elevated price inflation measures we are currently observing. All this additional spending and money is still rippling through the economy as much of it was not effectively sterilized. However, as time goes on, all of this spending is being captured by the largest firms as profit. This huge soaking up is still taking place. About the time that the covid stimulus was first announced in March and April of 2020, I instructed the reader to buy as many income generating assets as possible, because all of this sovereign debt generation would result in higher asset prices across the board. Compounding the misery for the average person is the fact that the Federal Reserve waited too long to attempt to control the growing price inflation that resulted.

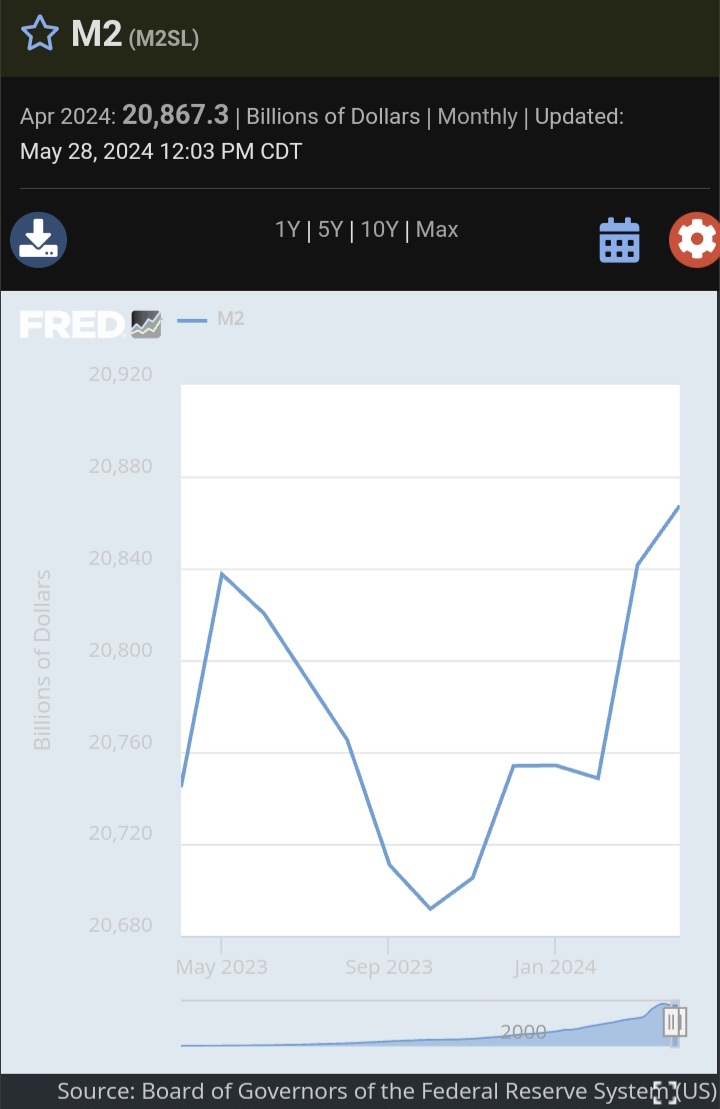

About the time that the covid stimulus was first announced in March and April of 2020, I instructed the reader to buy as many income generating assets as possible, because all of this sovereign debt generation would result in higher asset prices across the board. Compounding the misery for the average person is the fact that the Federal Reserve waited too long to attempt to control the growing price inflation that resulted. As the months move forward from here and the money stock measures stabilize, inflationary pressures should and have been coming down. Of course, we still have trillion dollar deficits, which must be financed with additional sovereign debt securities. These sovereign debt securities provide investors with collateral to purchase other assets, such as the national housing supply as well as equities and marquis businesses.

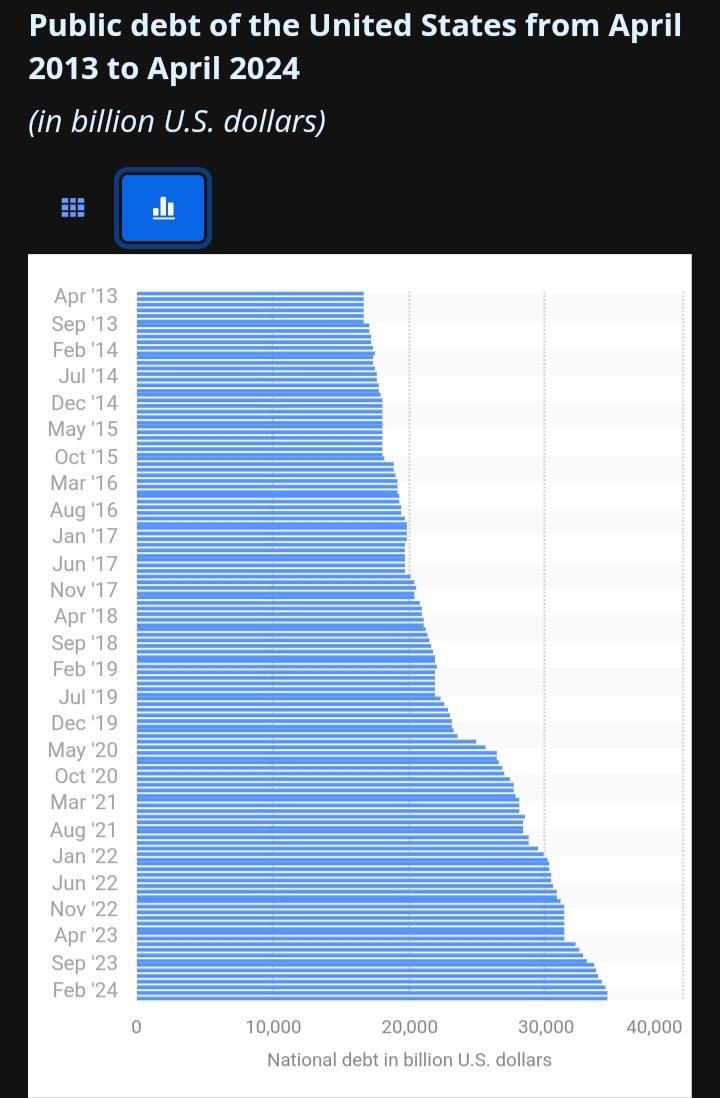

As the months move forward from here and the money stock measures stabilize, inflationary pressures should and have been coming down. Of course, we still have trillion dollar deficits, which must be financed with additional sovereign debt securities. These sovereign debt securities provide investors with collateral to purchase other assets, such as the national housing supply as well as equities and marquis businesses. With short-term interest rates remaining elevated, the level of federal government interest expenses continues to climb at a rapid pace. While the small saver can park money in Schwab’s money market fund at 5.2% and make some extra cash, the vast majority of this extra money the federal government is paying for its financing is going to the institutions. This essentially is another great transfer of wealth vehicle from the taxpayer and wage earner to the institution. As we can see, this interest expense has now crossed the trillion dollar threshold.

With short-term interest rates remaining elevated, the level of federal government interest expenses continues to climb at a rapid pace. While the small saver can park money in Schwab’s money market fund at 5.2% and make some extra cash, the vast majority of this extra money the federal government is paying for its financing is going to the institutions. This essentially is another great transfer of wealth vehicle from the taxpayer and wage earner to the institution. As we can see, this interest expense has now crossed the trillion dollar threshold. In essence, this is additional money that ends up in the pockets of the large institutions and it is being used to purchase more assets and consolidate the wealth. The wage earners are the last ones to see this extra money and by the time they see it, the cost of living has already increased to the point that any extra wage is spent. Those who see this money first are the ones who benefit. The asset owners benefit through higher levels of asset price appreciation and the ever increasing cash flows these assets generate. Stock owners have been richly rewarded as the Federal Reserve subsidizes this wealth transfer by suppressing bond yields. Existing homeowners benefit as the prices of their homes escalate.

In essence, this is additional money that ends up in the pockets of the large institutions and it is being used to purchase more assets and consolidate the wealth. The wage earners are the last ones to see this extra money and by the time they see it, the cost of living has already increased to the point that any extra wage is spent. Those who see this money first are the ones who benefit. The asset owners benefit through higher levels of asset price appreciation and the ever increasing cash flows these assets generate. Stock owners have been richly rewarded as the Federal Reserve subsidizes this wealth transfer by suppressing bond yields. Existing homeowners benefit as the prices of their homes escalate.

I am so grateful I began investing out near Strasburg, Winchester, and in Shenandoah County Virginia. This area is on fire because it is mostly Caucasian European and they have a long heritage. Conservative Caucasian money is bailing on the multicultural garbage dumps near DC and deploying it out here in droves. I now have six houses here and can’t wait to dump more PG County properties.

To wit, according to The Hill, the Shenandoah County School board reverted the names of two of their schools back to their former Confederate names before the blacks cried out to their debt slave owners for action.

“Confederate names make comeback, triggering lawsuits”

A Virginia school district was sued this week after it restored Confederate military names for two buildings, foreshadowing a broader battle that is heating up ahead of the election.

The Virginia NAACP sued the school board in Shenandoah County after it voted to change Mountain View High School to Stonewall Jackson High School and Honey Run Elementary back to Ashby Lee Elementary.

https://thehill.com/homenews/education/4722907-confederate-names-make-comeback-triggering-lawsuits/

Thanks for another thorough analysis keeping your readers up to speed… I’ve read this a few times and I’m not finished yet. Further to your comment re: finding buyers for US debt, notice the saviour being forecast in this article as the digitization of the dollar advances

https://x.com/MikeBenzCyber/status/1802413643793047866/photo/1

I just added this chart to the research article for clarity purposes.

https://www.terminaleconomics.com/wp-content/uploads/2024/06/M2UST.png